|

|

Riding

the double-dipper Riding

the double-dipper

Capitalist leaders are in disarray as they strive

and fail to get to grips with the eurozone crisis and its threat to the

global economy. Neither the G20 summit in Mexico, nor crisis talks in

Rome offered any solutions, as politicians and economists desperately

try to hang on to the eurozone roller-coaster. LYNN WALSH reports.

O NCE

AGAIN, THE eurozone crisis dominated the G20 meeting of world capitalist

leaders (Los Cabos, Mexico, 18-19 June). Yet again, the meeting

concluded with a bland communiqué with no concrete measures to tackle

either the eurozone crisis or the deepening global crisis. Barack Obama,

facing presidential elections in November, desperately called on the

eurozone leaders to resolve the debt crisis and temper austerity

measures with ‘growth policies’. European leaders, on the other hand,

noted that Obama has not been able to promote a further stimulus package

in the US because of Republican opposition in the Congress. Moreover,

they warned that the US’s own debt burden, with the threat of colossal

spending cuts in 2013, could push the US – and the world economy – over

the edge of the abyss.

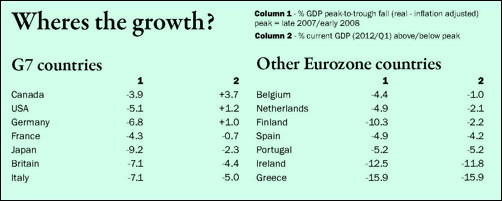

Only three of the G7 countries

(Canada, the US and Germany) have got back to their pre-crisis peak of

production (see table below). Now US growth is petering out, while there

is either stagnation or recession in the eurozone (with Germany now

sliding into recession). In 2007-08, the housing mortgage crisis

triggered a worldwide banking and financial crisis. Now the sovereign

debt crisis holds both European governments and the major banks in the

thrall of financial turmoil. Greece and Spain in particular are like

time-bombs which could detonate a major explosion at any time.

Source: Floyd

Norris, Cheer Up US, It Could Be Worse, International Herald Tribune, 16

June 2012

The Rome meeting (22 June) of the

leaders of the eurozone’s big four economies (Germany, France, Italy and

Spain) demonstrated that the eurozone crisis is no nearer to resolution.

They announced a €130 billion ‘growth package’, but with very limited

new money. They remained divided on the most acute issue, the continuing

credit crisis.

Mario Monti, François Hollande and

Mariano Rajoy called for the use of the eurozone’s bail-out funds to

"stabilise financial markets". They want to authorise the European

Financial Stability Facility (EFSF), and later the European Stability

Mechanism (ESM) to intervene directly to support shaky banks. They also

propose that the rescue funds should be able to buy the debt of

‘virtuous’ countries to support their bonds (presumably ‘virtuous’ means

any eurozone country except Greece). Angela Merkel, however, opposed

these proposals, once again highlighting the contradiction within the

eurozone between a common currency and the national interests of member

states.

"There was an agreement among all of

us", claimed Spain’s prime minister, Rajoy, "to use any necessary

mechanism to obtain financial stability in the eurozone". Responding to

Merkel’s call for accelerated steps towards a fiscal union, Hollande

said there could be "no transfer of sovereignty without an improvement

in solidarity", continuing to advocate the need for mutualisation of

eurozone debt, through eurobonds or some other mechanism. Solidarity,

responded Merkel, was possible only with serious controls and collective

oversight: "You cannot have guarantees without control".

"It’s not that I do not want to

provide help, but the treaties are set up in such a way that the

governments are the partners", Merkel said. In other words, the eurozone

(or the European Union for that matter) is an inter-governmental

organisation, not a federal state. Moreover, Germany has to finance

around 30% of any eurozone intervention, and has so far contributed

approximately €300 billion to the various bailouts. "Germany’s strength

is not infinite, its powers are not unlimited", protested Merkel in

Rome.

At the G20 meeting in Mexico, Obama

and Christine Lagarde, head of the International Monetary Fund (IMF),

were calling on the eurozone leaders to take urgent action to resolve

the crisis, which is increasingly becoming a drag on the world economy.

But even the terms of the bailout of the Spanish banks have not yet been

fully resolved. It was agreed for the eurozone to provide up to €100

billion to stabilise the Spanish banks. But there is no agreement on the

procedure. Rajoy, Hollande and Monti are calling for the funds to go

directly to the banks so they do not add to Spain’s sovereign debt

(which would further undermine the country’s credit rating).

Merkel, however, is insisting that

the bail-out funds are channelled through the Spanish government. This

explains why Spain’s borrowing costs remain well over 6% and have gone

over 7% a number of times (compared, for instance, with 1.45% for

France). Moreover, some eurozone leaders are insisting that the loans to

Spain from the EFSF or the ESM will have ‘seniority’. In other words, in

the event of default they will have priority as far as repayment is

concerned. This leads investors in the bond market to regard Spanish

debt as even more of a risk, as they are demoted when it comes to credit

or repayment in the event of default.

Like the low-cost, long-term credit

recently provided to European banks by the European Central Bank (ECB),

bail-out funds for the Spanish banks are likely to have a very limited,

short-lived effect on the crisis.

Up until quite recently, the ECB was

actively intervening to soften the eurozone credit crunch. It was buying

eurozone government bonds, which tended to keep borrowing costs lower

than they would otherwise be. Since June 2010, when the ECB started this

‘securities market programme’, the bank has bought €210.5 billion of

bonds. However, in recent weeks the bank stopped the SMP programme,

despite the fact that Spain’s bonds yields soared.

The ECB also launched the

Longer-Term Refinancing Operations (LTROs), allowing eurozone banks to

borrow huge amounts from the ECB at low interest rates (and on the basis

of a wide range of collateral). Among other things, this allowed banks

to buy government bonds, a backdoor way of the ECB supporting eurozone

governments. Early in June, however, the ECB changed its policy,

refusing to buy any more government bonds. ECB officials indicated that

they now regarded as the task of the EFSF and the ESM to buy eurozone

government bonds.

The ECB’s change of policy reflects,

among other things, the pressure of the German government and others who

oppose providing unlimited credit to debtor countries (as creditor

countries like Germany would have to pick up the bill).

The impasse of the eurozone is shown

by the ESM, which is still not up and running. In effect, Hollande,

Monti and others are proposing that (as the ECB does not act as a ‘bank

of last resort’, backing the debts of major governments) the ESM would

act as a bank, with powers to directly support floundering banks or

provide additional bail-out funds to eurozone governments. Merkel

opposes this. Moreover, the ESM has yet to be approved by the German

parliament, and this may be delayed for some time by a challenge to its

constitutional legality in the German constitutional court.

Merkel’s position reflects that of a

section of the German capitalists, who are increasingly resentful at

being called on to bail out the weaker economies (despite the advantages

that Germany gained from being within the eurozone). Recent opinion

polls show that 55% of German voters wish that Germany had kept the

Deutschmark. This opposition to the eurozone will grow in the coming

months.

In an editorial (22 June) the

Financial Times warned: "Clock ticking for the euro’s leaders". Among

other gloomy things for European capitalists, they point to the Greek

time-bomb: "Financial markets" (that is, big financial speculators)

"took scant relief in the victory of one Greek party [New Democracy]

that wants to renegotiate the country’s rescue deal over another [Syriza]

that wants to reject it outright".

The new prime minister, Antonis

Samaras, leader of New Democracy, is now demanding that the

implementation of austerity measures already agreed in return for two

bail-out packages should be postponed for two years. It is estimated

that this would require a further €20 billion in bail-out funds. On

this, as on everything else, the eurozone leaders are divided. Hollande

and others are in favour of giving Greece more time, while Merkel and

others are opposed to any relaxation of the austerity measures. In

reality, the only issue is timing: the debts piled on to Greece

supposedly to provide a way out of its debt crisis, are unsustainable.

Despite New Democracy’s narrow victory, there will be further explosive

movements of the Greek working class and middle class against the

barbaric austerity measures being imposed on the country.

If the big four cannot reach

agreement on crucial issues, there is no chance of the European Council

coming up with solutions. The election of Hollande in France has

strengthened the demand for less austerity and greater promotion of

growth, still implacably opposed by Merkel and her allies. This deadlock

means prolonged stagnation or another downturn, which in turn means

continuous political and economic crisis. Capitalist leaders fear the

breakup of the eurozone, which would have incalculable repercussions in

Europe and throughout the world economy. But the contradictory forces

bottled up in the eurozone are working in the direction of partial

breakup, if not total breakup somewhere down the line.

Gloomy global prospects

THE OUTLOOK FOR global capitalism is

indeed gloomy. Since April/May this year there have been growing

indications of a new downturn in the world economy. There are a number

of overlapping and interrelated elements of crisis:

The burden of debt:

The high level of public and private debt and attempts to reduce

debt (‘deleveraging’) is restricting the flow of credit and depressing

consumer demand and investment. For the OECD area, government budget

deficits averaged -2.1% during 1999-2008. In 2009 this shot up to -8.1%

and is still currently -5.3%. The aggregate national debt for the OECD

area has continued to increase, and is now 108.6% of GDP. Household debt

(gross debt-to-disposable income) is also very high. For the euro area,

for instance, the pre-boom level in 2000 was 85.3% but is now 107.9%.

Company debt continues to be high. For non-financial companies

(debt-to-GDP ratio) was 78.8% whereas it is now 96.8%. For financial

corporations the debt ratio is even higher: it was 269.1% in 2000 and is

now 381.7%. These figures are unsustainable on the basis of weak or

completely stagnant growth, and carry the threat of increasing defaults

in both the household and company sectors.

Mass unemployment:

Unemployment remains catastrophically high. This is an effect of the

downturn, but reinforces it through weakened consumer demand, reduced

tax revenues, and increased costs of unemployment benefits.

In the EU (27 states) there are 24.6

million unemployed men and women, of whom 17.4 million are in the euro

area (17). This is a jobless rate of 11% in the eurozone, 10% in the EU.

In a number of countries the situation is much worse: in Spain the

unemployment rate is 24.3%, in Greece 21.7%. Youth unemployment for both

these countries is a catastrophic 50%.

Global unemployment is a devastating

indictment of capitalism. According to the ILO there are now 200 million

jobless people internationally (up from 175 million in 2000). There are

75 million young people unemployed, an increase of four million since

2007.

The ILO director general warned (30

May) in coded language of the threat of a social explosion due to mass,

long-term unemployment, especially of the youth. "The austerity-only

course to fiscal consolidation is leading to economic stagnation, job

loss, reduced [social] protection, and huge human costs, undermining

those social values which Europe pioneered. While trying to reduce the

public debt, unsuccessfully by the way, a social debt is building up

that will also have to be paid".

Fiscal austerity:

The policy of ‘fiscal consolidation’, aiming at the short-term

reduction of budget deficits and accumulated national debt through

spending cuts and tax increases – especially taxes like VAT which hit

working-class consumers hardest – is depressing growth, especially in

Europe. "Fiscal austerity responses to deal with rising public debts are

further deterring economic growth, which in turn is making a return to

debt sustainability all the more difficult". (UN Update, World Economic

Situation and Prospects, mid-2012)

The UN economists responsible for

this report take a much more Keynesian view of the situation than most

European leaders: "On the fiscal front, the current policies in

developed economies, especially in Europe, are heading into the wrong

direction, driving the economies further into crisis and increasing the

risk of renewed global downturn. The severe fiscal austerity programmes

implemented in many European countries, combined with mildly

contractionary policies in others such as Germany and France, carry the

risk of creating a vicious downward spiral, with enormous economic and

social costs. Under current conditions, characterised by weak private

sector activity and poor investor and consumer confidence, simultaneous

fiscal retrenchment across Europe has become self-defeating as massive

public expenditure cuts will further push up unemployment, with negative

effects on growth and fiscal revenue".

Bank crisis and continued credit

squeeze: The banking crisis continues,

with a recent sharp fall in bank lending. Following the 2008 financial

sector crisis, the US banks were recapitalised (that is, their capital

reserves were built up) through the government’s TARP programme,

implemented in the dying days of the Bush regime and approved by Obama.

This bailout provoked enormous public anger in the US, but largely

stabilised the US banks. In Europe, on the other hand, the

recapitalisation has been partial and patchy. The ECB has relieved many

banks of a slice of their dodgy government bonds. Yet banks have been

recently using cheap ECB credit (under the LTROs) to buy more risky

government bonds. At the same time, under the new ‘Basel III’ banking

rules, the banks are forced to build up bigger capital reserves than in

the past. They have also become wary of lending either to business or to

other banks, and this has led to a recent tightening of the credit

squeeze.

According to a recent article in the

International Herald Tribune (5 June), worldwide bank lending has

plummeted: "International lending by global banks in the fourth quarter

of last year fell by the largest amount since the collapse of Lehman

Brothers in 2008, according to data released Monday by the Bank for

International Settlements… In total, financial firms cut foreign lending

by $799 billion in the last three months of 2011…" Around 80% of the

reduction came from the so-called interbank market where institutions

lend money to one another. "The pull back in credit, particularly

amongst banks themselves, is the latest effort by financial institutions

to reduce exposure to the global economic slowdown. It also raises

concerns that the unwillingness of banks to lend money to each other may

have an effect on the broader economy, as businesses are unable to

obtain new financing". The Basel III rules are aimed at making banks

more resilient to future financial crisis, but in the short run they are

compounding the immediate problems faced by the financial sector.

Big corporations hoard cash:

While some companies (especially small and medium) are hit by the credit

squeeze, big corporations internationally are hoarding cash rather than

investing it in new productive capacity. In the UK, non-financial

companies are estimated to be holding Ł731.4 billion of cash reserves.

In the eurozone, cash hoards are estimated at around €2 trillion, while

in the US non-financial companies hold more than $2 trillion in cash and

other liquid assets. The big corporations evidently cannot find

sufficient opportunities for profitable investment. This reflects a

growing trend since the end of the post-war upswing (1950-73). (See:

Corporate Cash Hoarders Stunt Growth, Socialism Today No.158, May

2012) Without investment by the major corporations, there will be no

growth, the current stagnation will continue, and it will become

increasingly difficult to reduce the burden of debt.

The price of oil and geopolitical

risk: The price of oil soared to around

$140 a barrel on the eve of the 2008 financial crash and then plummeted

in 2009-10. However, despite the stagnation of the world economy, the

oil price rose 40% to reach an all-time high average yearly price of

$111 a barrel in 2011, and rose even more in early 2012 (to around

$120p/b). This was due to a combination of continued demand from China,

Brazil, etc, on the one hand, and supply restrictions on the other,

particularly due to sanctions against Iran. Since then, demand has

slackened, and Opec has increased its output. Analysts at Credit Suisse

recently predicted that the oil price could decline to around $50 a

barrel this year. The decline in the oil price has already resulted in a

reduction of inflation. Oil prices also have a big effect on food

prices, because of transport and fertiliser costs, etc. Other commodity

prices have also declined because of weakening demand from China, which

will hit commodity producers like Brazil, Australia, Canada, etc.

However, sanctions against Syria, continued sanctions against Iran, and

the possibility of further upheaval in the Middle East could push up oil

prices again, even during a downturn.

World trade:

After recovering from a steep fall in 2009, world trade appeared to

rebound in 2010. It grew in real terms at an average of 6.7% a year

during 1999-2008, but plummeted to -10.7% in 2009. It recovered to 12.8%

in 2010, but fell to 6% in 2011, and is only expected to grow by around

4% this year. The World Trade Organisation (WTO) and other organisations

are sounding alarms about creeping protectionism. In April, the WTO

reported that since mid-October 2011, the G20 economies had added 124

new restrictive measures affecting about 1% of world imports. (Increase

in Barriers to Trade, New York Times, 22 June) Global Trade Alert, an

independent organisation, reports that "protectionist actions including

tariff increases, export restrictions and skewed regulatory changes were

much higher in 2010 and 2011 than previously thought, with many more in

the pipeline". (Protectionist Fears Highlighted, Financial Times, 14

June) "The world trading system", comments Global Trade Alert, "did not

settle down to low levels of protectionism after the spike in

beggar-thy-neighbour policies in 2009". In a period of economic

stagnation, or downswing, trade restrictions will become more and more

prevalent, reinforcing economic stagnation.

US recovery falters:

The US is one of the few major economies to have surpassed its 2008

peak. The peak-to-trough fall was -5.1% and, at the beginning of this

year, it was +1.2% above the previous peak. However, recovery has been

very weak and uneven, particularly regarding unemployment. After growing

3% in 2010, growth fell to 1.7% in 2011 and is showing signs of petering

out this year. Consumer spending, which accounts for around 70% of the

US economy, has been hit by the enormous losses in household income

suffered by millions of Americans. The Federal Reserve bank recently

reported that "the median family’s net worth dropped 38.8% during the

three-year period [2007-10]… the biggest drop in net worth since the

survey started in 1989". The average American still earns less than six

years ago, even allowing for inflation. (America Suffered Record Decline

in Wealth, Reuters, 11 June)

Recently, manufacturing activity has

slowed down, particularly in capital goods, reflecting the decline in

demand from Europe in particular, one of the US’s major markets. The

weak US recovery, moreover, has been a ‘jobless’ recovery. There are

officially 12.7 million unemployed workers in the US, with eight million

part-time workers who really need full-time jobs. Growth in (non-farm)

jobs averaged 226,000 in the first three months of 2012 but has slowed

to 73,000 in the last two months. The dismal news of only 69,000 jobs

being created in May was taken as a sign of renewed recession – and led

to a dip in world stock exchanges.

China slows:

The Chinese economy remained a locomotive of growth during the

global downturn. Its average GDP growth during 2006-09 was 11.4% and

remained at 10.4% during 2010. This was very largely due to the huge

stimulus package implemented by the regime. It is estimated by Gary

Shilling of Bloomberg that China’s stimulus package was the equivalent

of 12% of GDP (compared with the US stimulus in 2009 of 6% of GDP).

However, in the first quarter of this year, China’s growth fell to

around 8% and is expected to slow even further this year. This partly

reflects a tightening of credit by the regime last year to try to curb

inflation, but it also reflects the beginnings of a sharp decline in the

property bubble, and a decline in exports because of the slowing of the

world economy. A slowdown in China would reduce its demand for

commodities, leading to a general fall in commodity prices (already

underway), which would especially hit commodity exporters such as

Brazil, Australia, Canada, etc.

Chinese government officials admit

that official statistics underestimate the slowdown in output. Figures,

for instance, for electricity demand, which is a proxy for output

growth, indicate an even sharper slowdown. The Chinese regime has

loosened its credit policy and indicated that there will be new stimulus

measures. However, it is doubtful, given the huge debts accumulated on

the basis of the last stimulus package, that it will be on the same

scale as before. Moreover, this downturn coincides with the changeover

in the top party leadership (and follows the Bo Xilai scandal). Reduced

growth carries the threat of more intense political conflict within

China, which could in turn undermine growth even more. This would have a

profound effect on the global economy.

European stagnation/crisis:

The crisis in European capitalism has become a major factor in the

trend towards global downturn this year. The EU countries are likely to

tally zero growth this year, while the eurozone will experience negative

growth (currently predicted by the UN at -0.3% but probably deeper). At

the same time, the threat of a default by a major European country or

the fracturing of the eurozone (for example, through a Greek default)

has had a major effect on global financial markets. The decline in

demand for the exports of major economies like the US and China has had

a depressing effect on global output.

The limits of monetary policy:

In the absence of further stimulus policies (Obama’s proposals have

been blocked by the Republican-dominated Congress) capitalist

governments have relied on monetary policy, with low, near-zero interest

rates and huge injections of credit into the system. This has mainly

been done through the policy of ‘quantitative easing’ (QE), the

contemporary equivalent of printing money, and various other

‘unconventional’ monetary measures.

QE has been described as ‘monetary

morphine’, a drug that eases the pain, becomes addictive, but fails to

cure the underlying sickness. Ultra-expansionary monetary policy has

failed to produce growth, but it has probably prevented the world

economy from slipping into a major slump. However, the policy is subject

to diminishing returns.

The US Federal Reserve led the way

with over $2.6 trillion-worth of QE, through buying US government bonds

and other financial assets (such as securitised mortgages). However, the

Fed has come under increasing attack from Republican ‘inflation hawks’

who believe, contrary to current trends, that QE will lead to

accelerated inflation. This is unlikely in the next period, given

massive overcapacity in the global economy and the weakness of consumer

and investment demand. Ben Bernanke, the head of the Fed, has hesitated

to resort to more QE, preferring to rely on ‘Operation Twist’, the

replacement of short-term US government bonds by long-term bonds, which

is estimated to inject $267 billion into the economy through lowering

interest rates. The continued slowdown of the economy and lower

inflation, however, will almost certainly produce another round of QE in

the US.

The Bank of England has implemented

Ł325 billion of QE. As in the US, however, the bank has hesitated to

introduce a new round. Instead, it has recently offered a package of

cheap loans to banks (totalling Ł100bn) on condition they increase their

lending to businesses. No doubt, there will be more QE to come.

The ECB has avoided the term

quantitative easing, but nevertheless has implemented measures that are

very similar: €2 trillion of government bond purchases and cheap loans

to banks (under the LTROs). However, the ECB has recently stopped buying

eurozone government bonds in an effort to force the eurozone leaders to

activate the two rescue funds, the EFSF and the new ESM.

Expanding the money supply has been

described as ‘pushing on a piece of string’. If businesses are not

prepared to invest and consumers have no money to buy, a looser money

supply will not produce growth. This is admitted by Paul Tucker, a

deputy governor of the Bank of England, who recently said: "QE has

miserably failed to generate the sort of growth in broad money that the

bank has said it was targeting back in 2009". The massive expansion of

central banks’ balance sheets has failed to generate the sort of impact

on broad money that could be expected. (Paul Tucker, On Why QE Isn’t

Working, Financial Times, 13 June) Tucker advocates a broader monetary

policy, which would include the Bank of England buying up financial

assets (such as mortgages) that would pump money into businesses and

households.

A period of depression

WITHOUT FULLY RECOVERING from the

2007-09 slump, the world capitalist economy is sliding into a new

downturn. This stagnation is symptomatic of a depression, not as deep or

severe as the 1930s but, nevertheless, a period of weak investment and

growth, mass unemployment and increased tension between capitalist

rivals. The Financial Times columnist, Martin Wolf, describes it as a

"contained depression". (Panic Has Become All Too Rational, 5 June)

"Worse", he writes, "forces for another downswing are building, above

all in the eurozone. Meanwhile policymakers are making huge errors".

By this he means their insistence on

savage austerity measures which stand in the way of recovery. Hollande’s

modest proposals for a Keynesian-type stimulus package have been

described as a ‘faux pas’ by the Financial Times. His suggestion of

higher taxes on big business and the wealthy have been met with howls of

anguish.

Capitalist leaders are in complete

disarray. "What would happen", Wolf asks, "if a country left the

eurozone? Nobody knows. Might even Germany consider exit? Nobody knows.

What is the long-run strategy for exit from the crises? Nobody knows.

Given such uncertainty, panic is, alas, rational... Before now, I had

never really understood how the 1930s could happen. Now I do".

|